06.17.19

Worldwide spending on the Internet of Things (IoT) is forecast to pass the $1 trillion mark in 2022, reaching $1.1 trillion in 2023. A new update to the International Data Corporation (IDC) Worldwide Semiannual Internet of Things Spending Guide shows the compound annual growth rate (CAGR) for IoT spending over the 2019-2023 forecast period will be 12.6%.

“Spending on IoT deployments continues with good momentum and is expected to be $726 billion worldwide this year,” said Carrie MacGillivray, group VP, Internet of Things, 5G, and Mobility at IDC. “While organizations are investing in hardware, software, and services to support their IoT initiatives, their next challenge is finding solutions that help them to manage, process, and analyze the data being generated from all these connected things.”

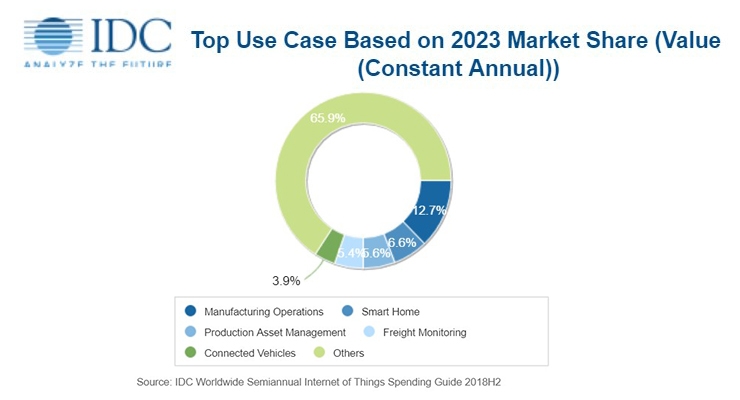

The three commercial industries that will spend the most on IoT solutions throughout the forecast are discrete manufacturing, process manufacturing, and transportation. Together, these three industries will account for nearly a third of worldwide spend total in 2023. The primary IoT use case for the two manufacturing industries will be manufacturing operations while transportation industry spending will largely go toward freight monitoring.

The consumer market will be the second largest source of IoT spending in 2019, led by smart home and connected vehicle use cases. With the fastest five-year growth rate across all industries (16.8% CAGR), the consumer market is forecast to overtake discrete manufacturing to become the largest source of IoT spending by 2023.

IoT services will be the largest technology category through the end of the forecast after overtaking hardware spending this year. Together, these two categories account for roughly two-thirds of all IoT spending. Services spending goes toward traditional IT and installation services as well as ongoing services such as content as a service. Hardware spending is dominated by module/sensor purchases. Software will be the fastest growing technology category with a five-year CAGR of 15.3% with a focus on application and analytics software purchases.

“Spending on IoT deployments continues with good momentum and is expected to be $726 billion worldwide this year,” said Carrie MacGillivray, group VP, Internet of Things, 5G, and Mobility at IDC. “While organizations are investing in hardware, software, and services to support their IoT initiatives, their next challenge is finding solutions that help them to manage, process, and analyze the data being generated from all these connected things.”

The three commercial industries that will spend the most on IoT solutions throughout the forecast are discrete manufacturing, process manufacturing, and transportation. Together, these three industries will account for nearly a third of worldwide spend total in 2023. The primary IoT use case for the two manufacturing industries will be manufacturing operations while transportation industry spending will largely go toward freight monitoring.

The consumer market will be the second largest source of IoT spending in 2019, led by smart home and connected vehicle use cases. With the fastest five-year growth rate across all industries (16.8% CAGR), the consumer market is forecast to overtake discrete manufacturing to become the largest source of IoT spending by 2023.

IoT services will be the largest technology category through the end of the forecast after overtaking hardware spending this year. Together, these two categories account for roughly two-thirds of all IoT spending. Services spending goes toward traditional IT and installation services as well as ongoing services such as content as a service. Hardware spending is dominated by module/sensor purchases. Software will be the fastest growing technology category with a five-year CAGR of 15.3% with a focus on application and analytics software purchases.