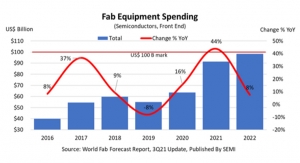

2021 is poised to mark a banner year for global fab equipment spending with 24% growth to a record $67.7 billion, 10% higher than the previously forecast $65.7 billion, and all product segments promising solid growth rates, according to the second-quarter 2020 update of the SEMI World Fab Forecast report.

Memory fabs will lead worldwide semiconductor segments with $30 billion in equipment spending, while leading-edge logic and foundry are expected to rank second with $29 billion in investments.

The 3D NAND memory subsegment will help power the spending spree with a 30% jump in investments this year before tacking on 17% growth in 2021.

DRAM fab investments will surge 50% next year after declining 11% in 2020, and fab spending on logic and foundry, mainly leading edge, will trace a similar but more muted trajectory, rising 16% 2021 after an 11% drop this year.

Some segments will see lower fab equipment spending but impressive change rates nonetheless. Image sensors will notch an impressive 60% increase in 2020 and add a 36% surge in 2021. Analog and mixed-signal will grow by 40% in 2020 and 13% in 2021. And power-related devices are forecast to register 16% growth in 2020 with a healthy jump of 67% in 2021.

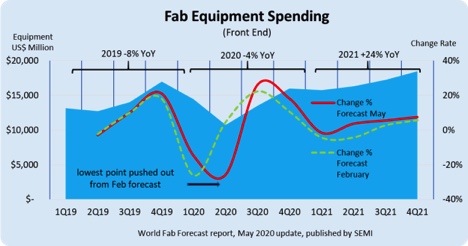

The SEMI World Fab Forecast report also shows the worldwide fab equipment spending trough in 2020 shifting from the first to the second quarter (see figure below).

A review of quarter-over-quarter (QoQ) spending trends reveals the impact of the COVID-19 pandemic over the course of 2020. Global fab equipment spending QoQ declined 15% in the first quarter of 2020 – performance that was stronger than the 26% decline forecast in February.

In March, some companies appeared to build up safety stock as a countermeasure to the spreading virus as shelter-in-place orders emptied offices, malls and schools worldwide. As the contagion grew, demand for IT and electronic products such as notebooks, game consoles and healthcare applications surged. Some stockpiling is expected to stretch into the second quarter, fueled by fear of restrictions – scheduled to take effect in late June – on semiconductor equipment sold to China.

While the World Fab Forecast report predicts rising investments in the second half of 2020, the year will mark the second consecutive yearly drop in fab equipment spending – 4% this year after an 8% dip in 2019.

And despite the bullish projections, threats from the pandemic still lurk. Pandemic-related layoffs, with more than 40 million workers idled in the United States alone (as of May), and company closures will trigger ripple effects in consumer markets and discretionary spending.

For instance, rising unemployment will lead to falling smartphone and new car sales. Despite those downdrafts, digital transformation and the need to communicate will still drive industry growth as cloud services, server storage, gaming and health applications spur demand for memory and IT-related devices.