Daniel Rogers, Head of Publishing, Smithers Pira08.16.17

Industrial and functional printing applications are all seeing growth with sectors including décor and laminates, ceramics, electronics, including displays and photovoltaics, glass, aerospace and automotive, biomedical, promotional and miscellaneous items, 3D printing and inkjet printed textiles. All of these are printed by a variety of specialist analog methods and inkjet.

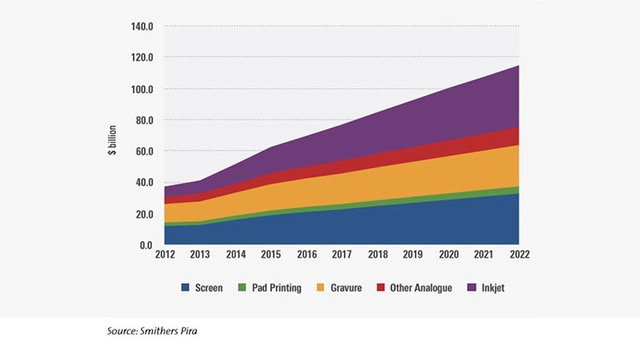

In ‘"The Future of Functional and Industrial Print to 2022," Smithers Pira values the current market at $76.9 billion, up from $37.2 billion in 2012, but with further growth forecasted to $114.8 billion by 2022.

“Suppliers have developed new equipment that widens the applications, with new inks, coatings and functional fluids providing new properties of flexibility, adhesion and durability, together with novel capabilities in electronics and biomedical to provide specific actions. While analog printing methods – gravure, flexo, litho, screen, pad printing and foiling – are widely used, there is very strong growth in digital methods, with new inkjet inks and fluids opening many new opportunities,” said Sean Smyth of Smithers Pira.

“These markets do not use paper or paperboard substrates, but rather plastic, film, glass, wood, metal, ceramics, textiles, laminates and composite materials are involved. In the case of 3D printing there are plastics and metals, with some composites,” he added.

Industrial printing takes place across the world, with manufacturers using the processes, and specialist suppliers selling to component and product manufacturers. Routes to market vary widely, with large manufacturers employing printing functions as part of their processes, and specialist print businesses supplying components.

Asia is the largest region, reflecting the concentration of manufacturing there, with large printing companies supplying electronics and environment materials, films and interior décor materials, and it is home to many giant electronic companies using printing as part of the manufacture of membrane switches, tags, circuitry, displays and photovoltaics.

There is also strong growth in North America and Western Europe for high-value items and as improvements to many manufacturing processes. New technologies are being developed in these regions, with inkjet textile bringing high-value, short-run textile printing closer to the end user, while 3D printing is enabling changes to some manufacturing while potentially changing business models and whole supply chains through distributed 3D printing on-demand. Printing may be used as part of a wider manufacturing process or, in the case of 3D additive printing, it can be the manufacturing.

The routes to market for printing are very complex and fragmented. Established suppliers may be manufacturers, or part of a wider supply chain. Often these companies will show less concern about the efficiency of a printing process when it is just one component of a manufacturing process. When building a car that sells for $30,000, an instrument panel that costs $100 is significant, but it is not a critical part of the cost build-up since print on that $100 panel will be worth $1-$2.

The demand for ever-increasing efficiency of printing technology does not play out in the same way – until print becomes a bottleneck or the end-use market demands change. Gravure, screen, pad printing and foiling are perfectly adequate for many of the long-established applications in which they are used. In producing a beer stein or sheet of exterior architectural glass, the printing is a small component of the process and often the decoration will be integrated in the manufacturing line. In a changeover, the print setup is generally a lot simpler than the product change.

The required skillset for this print is probably less than in commercial print or packaging; prepress production is often outsourced with screens, plates and cylinders bought in as required and reused over many years. The management of the industrial plant will concentrate on improving the methods of making the product rather than the intricacies of print technology. There is also much activity in developing routes to market, for print suppliers and equipment manufacturers, and for associated consumables supply.

The industrial print sector is growing and this represents attractive market opportunities for the beleaguered commercial graphics and publication print sector, together with their equipment and consumable suppliers. Print service providers have become more efficient in print production, developing workflows and lean manufacturing. Digital technology is widely used and some of these developments are being adopted by industrial print suppliers who are examining the potential and implications of digital, particularly inkjet print.

There is consistent growth across most industrial functional print markets and regions, including the established analogue print processes. Growing demand reflects increasing demand for construction, automotive and those manufactured products that are increasingly incorporating print. This is in contrast to the commercial graphics and publication print sector, which is seeing a significant fall in demand for print. Many of those established equipment and consumable suppliers are looking for alternative markets and industrial print growth is very attractive to them, as it is to print service providers.

Smithers Pira is a worldwide authority on packaging, paper and print industry supply chains. Established in 1930, Smithers Pira provides strategic and technical consulting, testing, intelligence and events to help clients gain market insights, identify opportunities, evaluate product performance and manage compliance. The Future of Functional and Industrial Print to 2022 is available for £4,500. For more information visit www.smitherspira.com.

In ‘"The Future of Functional and Industrial Print to 2022," Smithers Pira values the current market at $76.9 billion, up from $37.2 billion in 2012, but with further growth forecasted to $114.8 billion by 2022.

“Suppliers have developed new equipment that widens the applications, with new inks, coatings and functional fluids providing new properties of flexibility, adhesion and durability, together with novel capabilities in electronics and biomedical to provide specific actions. While analog printing methods – gravure, flexo, litho, screen, pad printing and foiling – are widely used, there is very strong growth in digital methods, with new inkjet inks and fluids opening many new opportunities,” said Sean Smyth of Smithers Pira.

“These markets do not use paper or paperboard substrates, but rather plastic, film, glass, wood, metal, ceramics, textiles, laminates and composite materials are involved. In the case of 3D printing there are plastics and metals, with some composites,” he added.

Industrial printing takes place across the world, with manufacturers using the processes, and specialist suppliers selling to component and product manufacturers. Routes to market vary widely, with large manufacturers employing printing functions as part of their processes, and specialist print businesses supplying components.

Asia is the largest region, reflecting the concentration of manufacturing there, with large printing companies supplying electronics and environment materials, films and interior décor materials, and it is home to many giant electronic companies using printing as part of the manufacture of membrane switches, tags, circuitry, displays and photovoltaics.

There is also strong growth in North America and Western Europe for high-value items and as improvements to many manufacturing processes. New technologies are being developed in these regions, with inkjet textile bringing high-value, short-run textile printing closer to the end user, while 3D printing is enabling changes to some manufacturing while potentially changing business models and whole supply chains through distributed 3D printing on-demand. Printing may be used as part of a wider manufacturing process or, in the case of 3D additive printing, it can be the manufacturing.

The routes to market for printing are very complex and fragmented. Established suppliers may be manufacturers, or part of a wider supply chain. Often these companies will show less concern about the efficiency of a printing process when it is just one component of a manufacturing process. When building a car that sells for $30,000, an instrument panel that costs $100 is significant, but it is not a critical part of the cost build-up since print on that $100 panel will be worth $1-$2.

The demand for ever-increasing efficiency of printing technology does not play out in the same way – until print becomes a bottleneck or the end-use market demands change. Gravure, screen, pad printing and foiling are perfectly adequate for many of the long-established applications in which they are used. In producing a beer stein or sheet of exterior architectural glass, the printing is a small component of the process and often the decoration will be integrated in the manufacturing line. In a changeover, the print setup is generally a lot simpler than the product change.

The required skillset for this print is probably less than in commercial print or packaging; prepress production is often outsourced with screens, plates and cylinders bought in as required and reused over many years. The management of the industrial plant will concentrate on improving the methods of making the product rather than the intricacies of print technology. There is also much activity in developing routes to market, for print suppliers and equipment manufacturers, and for associated consumables supply.

The industrial print sector is growing and this represents attractive market opportunities for the beleaguered commercial graphics and publication print sector, together with their equipment and consumable suppliers. Print service providers have become more efficient in print production, developing workflows and lean manufacturing. Digital technology is widely used and some of these developments are being adopted by industrial print suppliers who are examining the potential and implications of digital, particularly inkjet print.

There is consistent growth across most industrial functional print markets and regions, including the established analogue print processes. Growing demand reflects increasing demand for construction, automotive and those manufactured products that are increasingly incorporating print. This is in contrast to the commercial graphics and publication print sector, which is seeing a significant fall in demand for print. Many of those established equipment and consumable suppliers are looking for alternative markets and industrial print growth is very attractive to them, as it is to print service providers.

Smithers Pira is a worldwide authority on packaging, paper and print industry supply chains. Established in 1930, Smithers Pira provides strategic and technical consulting, testing, intelligence and events to help clients gain market insights, identify opportunities, evaluate product performance and manage compliance. The Future of Functional and Industrial Print to 2022 is available for £4,500. For more information visit www.smitherspira.com.